Ask any room of banking executives how many have increased their AI investment over the past two years. Nearly every hand goes up.

Now ask how many can say their customers are significantly more satisfied with their digital experience than they were two years ago.

Most hands drop.

That gap — between what banks are spending on AI and what customers are actually experiencing — is what we call the Last Mile Problem. And it’s costing the industry more than most leaders realize.

The Investment Paradox

The scale of AI investment in financial services is staggering.

McKinsey estimates generative AI could unlock $200 to $340 billion annually for global banking. The average bank is already spending $22 million per year on GenAI initiatives, a figure growing at a 32% CAGR. And yet: MIT’s 2025 State of AI in Business report found that 95% of enterprise AI pilots fail to deliver ROI.

J.D. Power’s 2025 Banking Mobile App Satisfaction Study tells a very specific story about why. Virtual assistant usage in banking apps has declined — not stagnated, declined — from 33% to 30%. Customer satisfaction scores dropped from 691 to 687 out of 1,000. J.D. Power’s own explanation: customers now use ChatGPT daily. When they come back to your app, the experience gap is visible.

The money is flowing into Customer Data Platforms, AI Operations infrastructure, and data lakes. The intelligence being generated is real. But when a customer opens your app, they still see a static menu, a list of tabs, and a generic product page that bears no relationship to who they are or what they actually need.

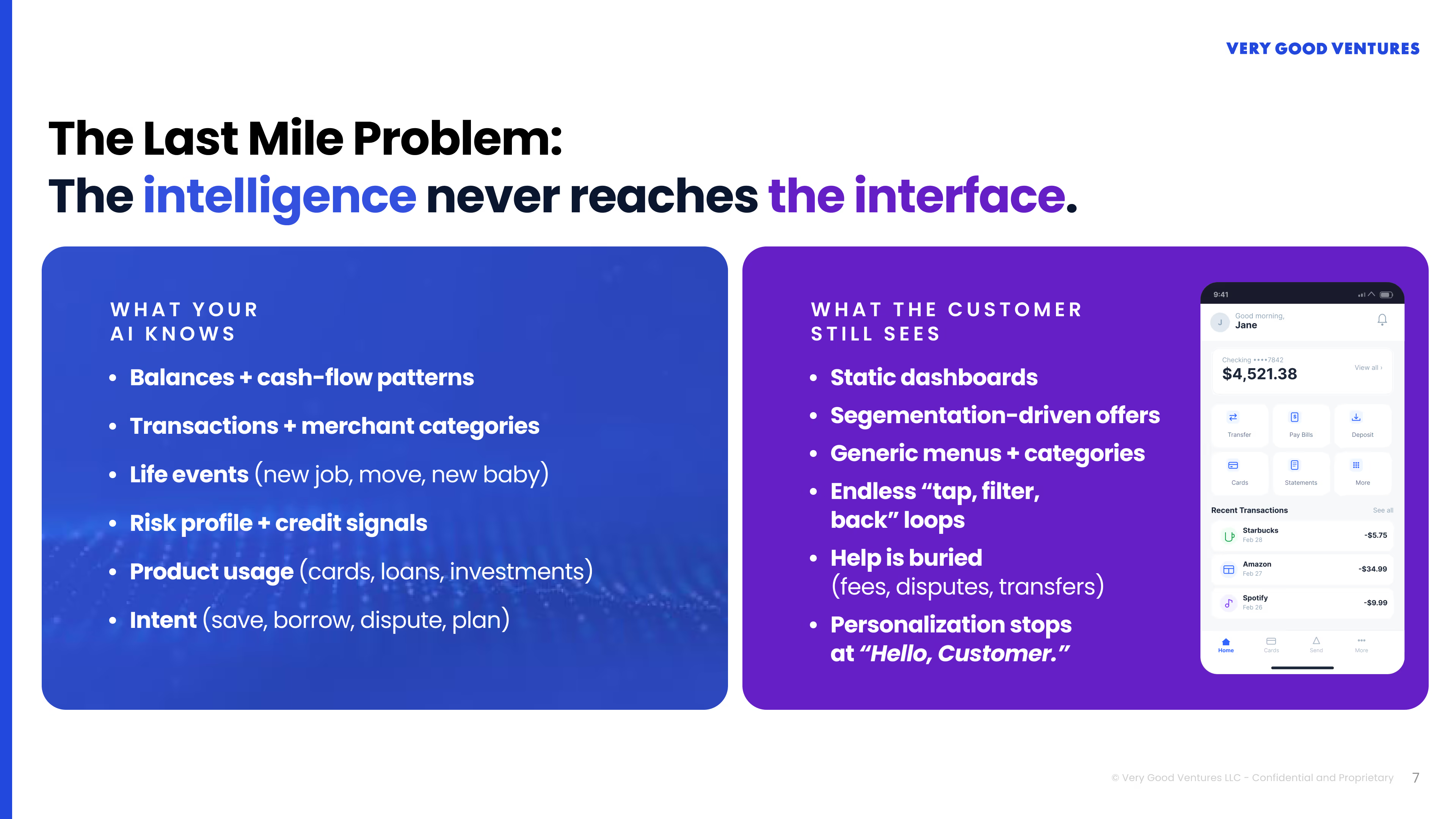

What Your AI Knows. What Your Customer Sees.

This is the Last Mile Problem.

Consider the data advantage banks already hold. Your systems know each customer’s balances and cash-flow patterns. Transaction history and merchant categories. Life events — a new job, a recent move, a new baby. Risk profile and credit signals. Intent signals from browsing behavior.

But when a customer opens your mobile app, they see: a static dashboard, segmentation-driven offers that could apply to anyone, a generic menu of categories, and feature help buried behind three taps.

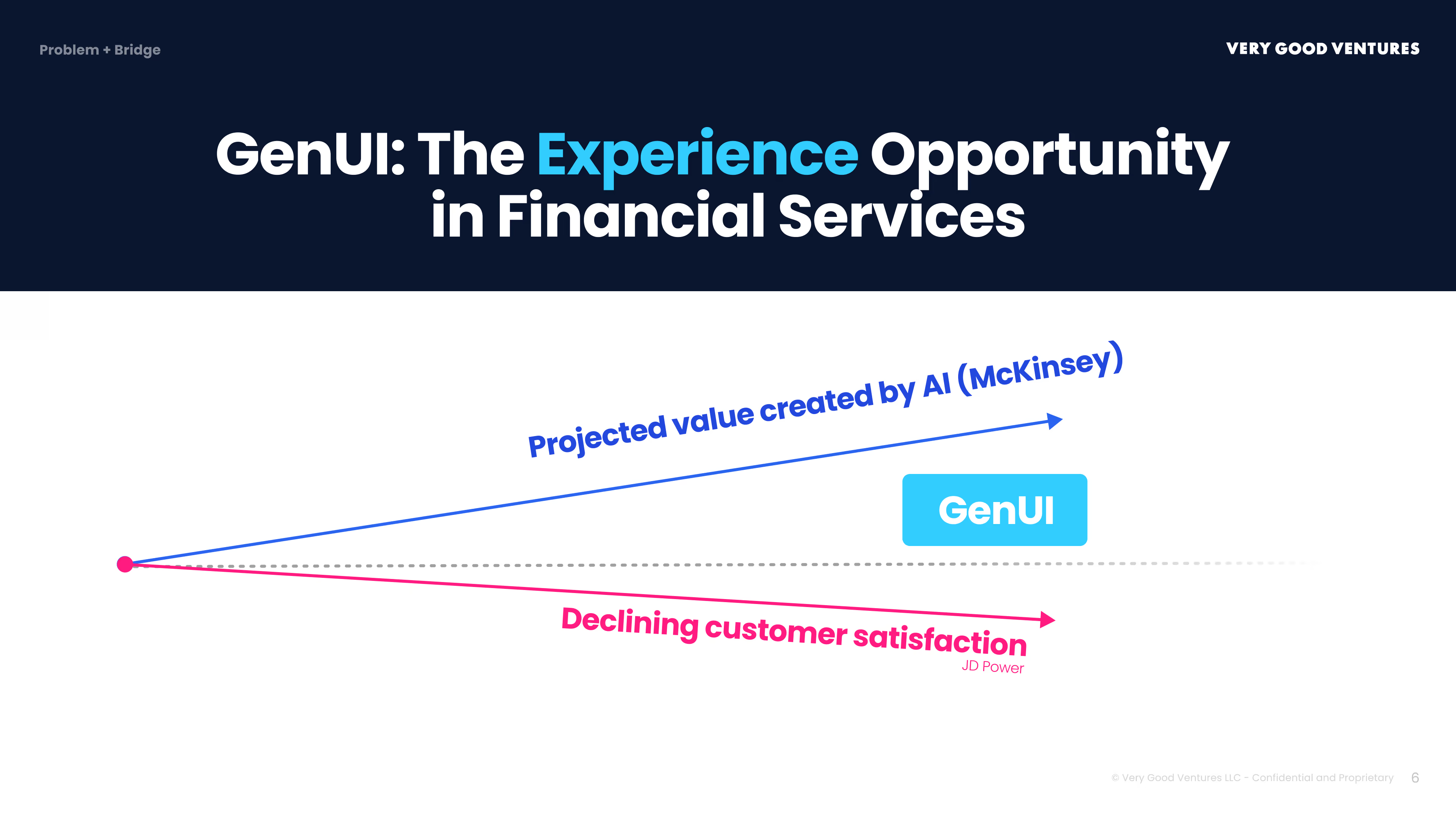

AI investment is projected to unlock hundreds of billions in value. Customer satisfaction is moving in the opposite direction. GenUI is the bridge.

Accenture research shows personalization drives a 10–20% revenue lift in financial services. We know it works. Most institutions simply can’t capture it at the screen level. The intelligence never reaches the interface.

Now here’s what closing that gap looks like in practice — the same bank, the same app, completely different experiences built in real time for two different customers:

Same bank. Same app. Completely different home screens, assembled in real time based on each person’s profile, goals, and life situation. This is what closing the Last Mile looks like.

Finding the Highest-Impact Starting Point

Understanding that GenUI can personalize the interface is one thing. Knowing where to start is another. Most institutions have dozens of potential use cases on a whiteboard somewhere. Competing priorities, legacy constraints, and a board asking for ROI proof make the prioritization question real.

Rather than guessing, VGV used our Opportunity Map framework — a proprietary methodology built on Anthony Ulwick’s Jobs to Be Done research.

The Research

We conducted in-depth interviews with banking customers who were actively considering opening a new account but had not yet progressed. The goal was to uncover the jobs these customers needed to complete in order to feel confident moving forward.

Three jobs emerged consistently:

- Understand what I would actually gain — not marketing copy, but real clarity about how a specific account fits my specific financial situation

- Compare options without getting lost — customers felt overwhelmed trying to evaluate products, benefits, and tradeoffs across multiple offerings

- Complete the process without friction — every extra step, every re-entry of information, every form that doesn’t auto-populate is a reason to quit

These are not new insights. They have been sitting in your NPS data for years. What’s new is what we can now do about them.

The Opportunity Map

We plotted each job against two inputs: how important it is to customers, and how satisfied they currently are with how their bank supports it. Where importance is high and satisfaction is low — that gap is the opportunity score.

Look at the far left of the map.

The biggest opportunity across the entire account-opening journey sits right at the start: helping customers understand what they'd actually gain by opening a new account in the first place — and making that value personal to their specific life situation. High importance. Low satisfaction. This is where the gap is largest, and where GenUI can move the needle fastest.

This job ranked as highly important across all customer segments — yet existing digital experiences left it nearly unserved. Customers wanted clarity and relevance. Instead, they were met with generic product descriptions and marketing language that could apply to anyone.

The average account-opening abandonment rate has doubled to 67% for some banks. Abandonment exceeds 50% when the process takes more than three to five minutes. Customers aren’t abandoning because the application is too hard. They’re abandoning before they even reach it — because no one has convinced them the account is right for them.

GenUI in Action: Guiding a Customer to Account Opening

What does GenUI look like at this specific moment in the journey? The demo below shows a bank using LLM-generated UI elements to guide a customer through exactly this job.

Notice what the bank is doing here. Rather than dropping the customer into a product catalog, the LLM first guides them through a series of savings scenarios — asking about their goal, their timeline, and what tradeoffs matter to them. Only once those scenarios are personalized to the customer’s actual life situation does the system surface an account recommendation. The AI isn’t presenting options; it’s building understanding first, then translating that understanding into a specific, justified recommendation.

This is the key distinction between GenUI and traditional personalization. It is interpreting intent — “I want to start saving for my daughter’s college fund” — and assembling a flow-based experience in real time: a context bar that updates as the conversation progresses, visual UI components that surface precisely when the customer needs them, and a comparison surface that appears exactly when the customer faces a complex decision.

The bank controls what the AI can do — the approved components, the compliance rules, the brand guardrails. The AI decides how to assemble those components, for this customer, in this moment.

GenUI is the experience layer where your AI investment finally becomes visible to customers.

Learn more about Generative UI at VGV